by Pam Martens and Russ Martens at Wall Street on Parade

On May 1, the Federal Deposit Insurance Corporation announced that First Republic Bank had failed and that it was being sold to JPMorgan Chase. At the time, JPMorgan Chase was already the largest and riskiest bank in the United States. The sweetheart deal the bank got from the FDIC to take over First Republic included the FDIC eating 80 percent of any losses on single-family residential mortgages for 7 years and 80 percent of any losses on commercial loans, including commercial real estate, for five years. The FDIC also provided JPMorgan Chase with a $50 billion, five-year fixed-rate loan at an undisclosed interest rate.

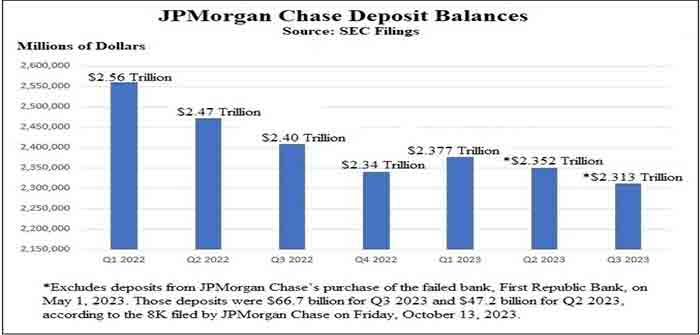

According to the filing that JPMorgan Chase made with the Securities and Exchange Commission last Friday, the deal also gave JPMorgan Chase something that it desperately needed: deposits. According to the 8-K filing that JPMorgan Chase made with the SEC on October 13, the acquisition of First Republic Bank added $47.2 billion to its deposit base in the second quarter and $66.7 billion in deposits in the third quarter.

As the chart above indicates, JPMorgan Chase suffered outflows of deposits in every quarter of 2022. It got a brief respite from inflows of deposits in the first quarter of 2023, as a result of the March banking panic that impacted smaller banks, then outflows took hold again. Excluding the deposits from First Republic Bank, JPMorgan Chase has lost $248.38 billion in deposits over the span of the last seven quarters. One doesn’t expect that at a bank that continues to trumpet its “fortress balance sheet.”

Even including the large amount of deposits that JPMorgan Chase gained from scooping up First Republic, the bank still bled $19.4 billion in overall deposits between the second quarter of this year and the end of the third quarter on September 30, according to JPMorgan Chase’s SEC filing on Friday, October 13.

Adding to the appearance of desperation at JPMorgan Chase…

Continue Reading