by Tyler Durden at ZeroHedge

There is no other way to describe today’s market carnage than a market in turmoil where things are rapidly breaking as the sudden disappearance of Russia’s “toxic” commodity collateral is suddenly sparking contagion and widespread liquidations.

With S&P futures a one way elevator lower after a modest rip higher on Ukraine ceasefire optimism early in the session, sending spoos more than 120 points down from session highs and closing down 2.9%, below 4,200, its worst close since October 2020…

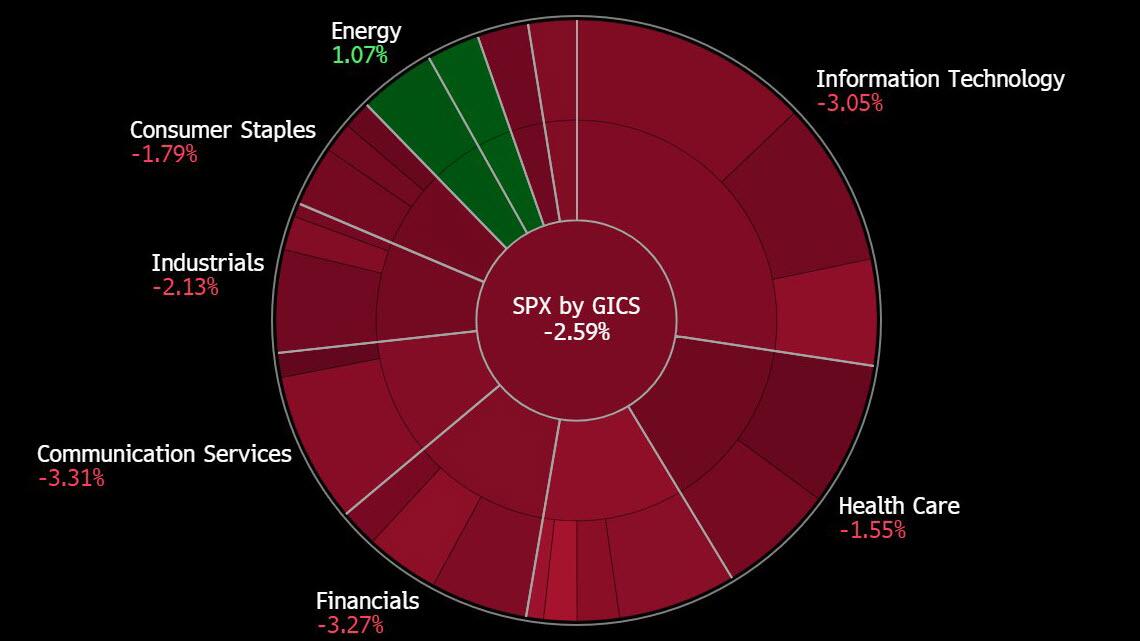

… and the Dow tumbling more than 800 points, everything was in the red, with the exception of the defensive utility sector and of course energy which is basking in the glow of a historic surge in the commodity space.

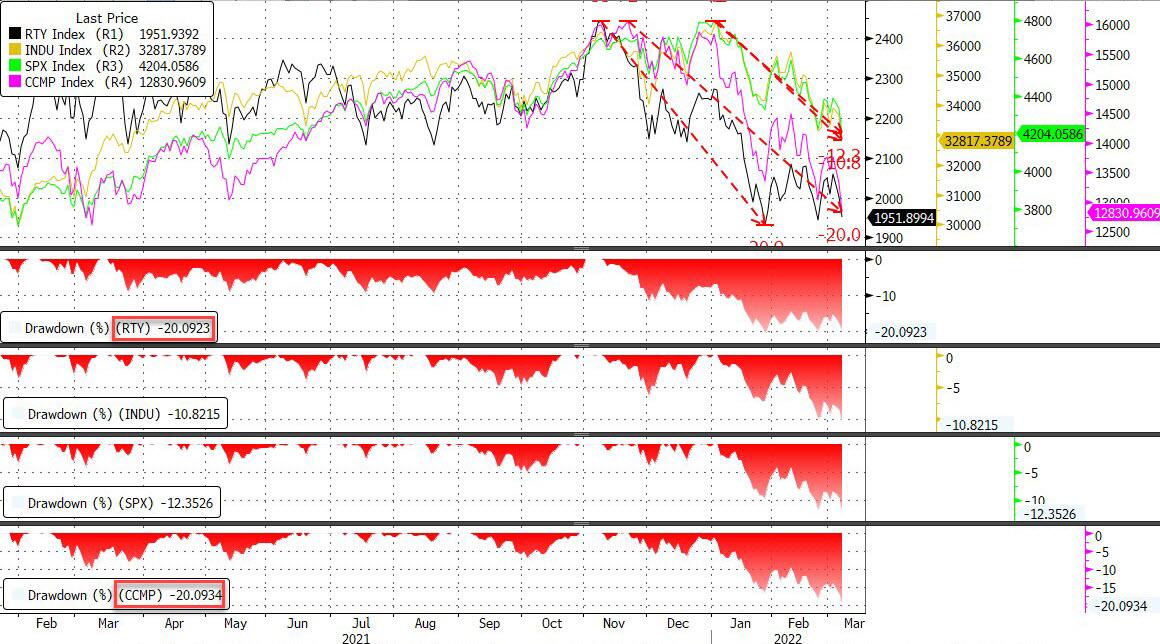

The Nasdaq tumbled 3.6% with the help of Facebook and Moderna both of which have wiped out more than 50% of their value from all time highs, and is now down more than 20% from its all time high, closing in a bear market, where it joins the Russell, which is now also down more than 20% from ATH.

Consumer discretionary stocks, with a decline of more than 3%, led the S&P 500 to a fresh session low. Companies with outsize exposure to Europe – Calvin Klein owner PVH and Ralph Lauren – were among SPX stocks with the biggest drops, while Amazon and Apple are among top decliners on a points basis. Higher energy costs and soaring food prices may crimp consumer spending in other areas, with oil posing a particular challenge. Consumer discretionary stocks are the worst performers among SPX sectors this year, shedding ~19% while the broader index falls ~11%.

While energy was the best – and only outperforming – sector, a testament to today’s dismal risk off mood is that the small-cap Russell actually outperformed both the S&P and the Nasdaq, with the latter tumbling more than 3%…

Continue Reading