by Tyler Durden at Zerohedge

One week after the biggest, and most spectacular hedge fund collapse since LTCM, we now have an (almost) clear picture of how Bill Hwang’s Archegos family office managed to single-handedly make a boring media stock the best performing company of 2021, but then when its luck suddenly ended it was margin called into extinction, leading to billions in losses for the banks that enabled what Bloomberg has dubbed its “leveraged blowout.”

Thanks to detailed reports by the Financial Times and Bloomberg, we now have the missing pieces to complete the picture of the biggest hedge fund implosion of the 21st century.

As a reminder, and as we previously discussed, we already knew how Archegos was building up stakes in its various holdings: unlike most other investors, the fund never actually owned the underlying stock or even calls on the stock, but rather transacted by purchasing equity swaps known as Total Return Swaps (TRS) or Certificates For Difference (CFD). Similar to Credit Default Swaps, TRS exposed Archegos to the daily variation margin on the underlying stock, and as such while the fund would benefit economically from increases in the underlying stock price (and, inversely, would be hit by price drops forcing it to put up more cash as margin any day the stock price dropped) it would never be the actual owner of record of the underlying stock. Instead, the stock that Archegos was long would be “owned” by its prime broker, the same entity that allowed it to enter into TRS in the first place. As such Archegos also never had any disclosure requirements, allowing it to transact completely in the dark while being fully compliant with SEC disclosure requirements – since it didn’t own the underlying stock, Archegos did not have to disclose it. Simple and brilliant.

This part is important because the lack of a documented trail of ownership to Archegos is what enabled the entire Ponzi bezzle… and the staggering leverage the fund applied to its portfolio. Furthermore, well aware that there was almost no way to verify just how much of a given stock he owned, Hwang proceeded to have nearly identical positions with not one, not two but at least eight prime brokers (the final number is still being determined as more and more come out of the woodwork).

Not that Archegos prime brokers were completely clueless as to what was going on.

As Bloomberg reports, while much of the investing world watched in stunned silence how an “old media” company – ViacomCBS – shot up almost 300% in weeks, becoming the best performing stock in the S&P500 and prompting investors to speculate that the stock was was either undervalued, or like GameStop, or a takeover target, a handful of execs at Wall Street’s top trading firms were aware of what was behind the move: it was Archegos Capital Management, who was building a massive position in ViacomCBS and a handful of other stocks… using leverage the same banks so generously offered with stock which the banks themselves technically owned!

But while banks around the world – from Goldman, Morgan Stanley and Wells in the US, to Credit Susse, UBS and Deutsche Bank in Europe, to Nomura and Mitsubishi UFJ in Japan – kept giving Hwang the leverage he needed to acquire more and more of the stock, until he became the biggest economic if not registered owner of Viacom, what they did not know – thanks to the was Total Return Swaps are structured – was the full extent of his wagers. Which were massive: he stealthily amassed $10 billion of Viacom.

Viacom was just one of many: using even more TRS and even more leverage across even more Prime Brokers, Archegos was able to place colossal wagers while avoiding the disclosures required of most investors. And so “almost invisibly” Hwang accumulated a portfolio which according to Bloomberg sources was as much as $100 billion!

Eventually, Archegos built positions in at least nine stocks that were big enough to rank him among the largest holders, fueled by a level of bank leverage that would have been unusual even for a hedge fund.

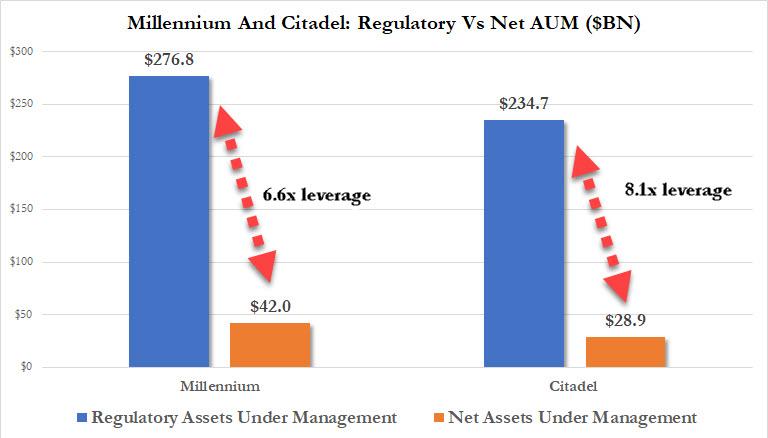

While we previously discussed the leverage aspect of Archegos strategy, here it is again: with Bill Hwuang managing approximately $10BN in assets under management, the multiple Total Return Swaps with unwitting prime brokers allowed the fund to build up a staggering $100 billion in positions, implying a huge 10x leverage. This is the kind of leverage one associated with the likes of financial titans like Citadel and Millennium, not a smallish family office which has zero downside protection (as we would eventually learn).

What is amazing about this unilateral Ponzi scheme is that it relied on what we have dubbed rehypothecated leverage: the fund never even owned the underlying stock which was layered with billions in generous Prime Broker debt, but it was Archegos’ Prime Brokers who not only would own the actual stock but would also allow Hwang to add tens of billions in leverage… on an asset that they owned!

What is also remarkable is that Archegos’ ponzi scheme could have continued indefinitely if only Viacom stock had i) continue to rise or ii) avoided a crash. After all, having ignited the initial upward moment, Archegos had effectively forced benchmark-tracking investors, exchange-traded funds, CTAs and other momentum investors to buy as well.

Sadly for Hwang (and his Primer Brokers) the upward momentum ended with a bang last Monday, when with its shares trading at $100, Viacom announced a $3BN stock sale, which hammered the stock, followed by a round of analyst downgrades, which sent the stock tumbling. It was at this point that Archegos was now facing tens of billions in margin calls on its VIACA Total Return Swaps from its Prime Brokers.

And therein lies the rub, because when the time came to unwind the Archegos Ponzi, the Prime Brokers’ counterparty was not Archegos but other Prime Brokers. This is what led to the infamous meeting late last Thursday, where a bunch of PBs tried to reach an amicable resolution ahead of Friday’s bloodbath. As Bloomberg adds, at several points during those exchanges, bankers implored Hwang to buy himself breathing room by selling some stocks and raising cash to post collateral. But “he wouldn’t budge.”

As a result, Morgan Stanley and Goldman promptly started dumping blocks of stock backing Archegos TRS in the open market. In doing so the started a margin call liquidation, in which those who sold first – like Goldman, Morgan Stanley and Deutsche – would avoid massive losses, while those who waited like Nomura and Credit Suisse… would not. Indeed, we already knew that Nomura, Japan’s largest investment bank, said its losses could hit $2Bn, while losses at Credit Suisse could be as large as $4Bn according to the FT.

At this point, many questions popped up, especially (and belatedly) inside the banks themselves: as the FT reports, executives within the prime brokerage divisions of at least two banks “are being quizzed by risk managers over why they offered a business as small as Archegos tens of billions of dollars of leverage on trades in volatile equities through swaps contracts,.”

As the FT further notes, echoing what we said above, while prime brokerage clients typically provide few details about their other trading activities, “executives from at least two of the six banks are investigating whether Hwang deliberately misled them or withheld vital information about mirror positions he had built up at rival banks, according to people involved in the probes.”

Well, no: Archegos did not mislead anyone. He simply used (and abused) a system where – as we put it – one investor can create as much rehypothecated leverage as the investors’ banks and Prime Brokers will allow him. In this case we know the number may have been as high as a mindblowing $90 billion.

Naturally, had the banks known that in a worst case scenario they would be facing other banks – since such replicated, or rather rehypothecated position would magnify the risks on each of the trades making a bank less likely to extend so much credit against them – none of this would have been possible. However, as long as everything was going up, and all of Archegos positions were pleasasntly surging nobody seemed to care… or bother to calculate just how big the downside risk was (one can thank the Fed Put for that).

One final remarkable aspect of this whole story is that this is not Hwang’s first crisis. In 2012 he submitted a guilty plea on behalf of his hedge fund to a charge of wire fraud, and he resolved related civil claims of insider trading without admitting or denying wrongdoing. Archegos is the family office he formed after winding down that firm, Tiger Asia Management.

However, as if nothing had ever happened, prime brokerages immediately began lining up to help the new business. Morgan Stanley was among his early backers. Deutsche Bank signed him as a client at the urging of at least one senior executive, according to Bloomberg, “who was unperturbed by the insider-trading taint and didn’t believe Hwang had done anything wrong, according to a person familiar with that decision.” Ironically, just a few years later, Hwang did something wrong and it would prove to be the biggest hedge fund collapse in post-LTCM history.

Not every bank acted like an idiot: one firm resisted the lure. Archegos approached JPMorgan sometime between 2016 and 2018 and was rebuffed, according to the Bloomberg report. At the time, JPMorgan was still revamping the equity prime-brokerage unit it had acquired with Bear Stearns during the 2008 financial crisis. “Dumb luck or not, the bank dodged a bullet.”

* * *

The rest of the story is mostly known, so now what.

Well, as we first hinted and as Bloomberg reports, already regulators are dropping hints of new rules to come, with SEC officials signaling to banks that they intend to make trading disclosures from hedge funds a higher priority, while also finding ways to address risk and leverage.

Senior finance executives acknowledge that a crackdown of some form, whether on borrowing or transparency or both, is inevitable.

Amusingly, and picking up on the FT’s reporting, Bloomberg also notes that while some of those firms have disclosed the financial impact of their roles in the Archegos collapse, none is willing to comment on how or why they enabled Hwang to become such a force in the market. After all what can they say: “the other guys vetted him, so we assumed he was clean”…

There are also questions whether Hwang’s counterparties knew about his relationships with other banks and the scale of the leverage he was using for what appear to be concentrated positions in a handful of companies. And – more ominously – if they did not know anything about his exposure, why the hell not? As we reported on Tuesday, JPMorgan (which successfully managed to avoid this scandal completely) estimated that the Prime Brokers facing Archegos may end up absorbing as much as $10 billion in combined losses.

Already credit rating agencies have downgraded outlooks for Credit Suisse and Nomura, citing concerns over “the quality of risk management” while activist investors are demanding better governance and would not mind if senior execs were summarily fired over this episode to restore confidence.

“Risk controls still are not where they should be,” David Herro, one of Credit Suisse’s biggest shareholders, said Wednesday in a Bloomberg TV interview. “Hopefully, this is a wake-up call to expedite the cultural change that is needed in this company.”

But going back to Bloomberg’s original point, for all their silence the prime-brokerage units of Nomura, Goldman Sachs, Morgan Stanley, Credit Suisse and others, had clues about what Archegos was doing. These firms knew about the trades they had financed, of course, and also had some visibility into his total borrowings. And yet they didn’t bother to ask about what, if any, risk management was being implemented to avoid an uncontrolled unwind. Or rather, the questions emerged only after the margin call.

What the Prime Brokers also didn’t know is that Hwang was taking parallel positions at multiple firms, piling more leverage onto the same few stocks, which brings us back to our rehypothecated leverage concept which we are confident we will use much more in the coming months, especially since “unwinding a series of large, leveraged bets placed by a single account is one thing; doing so when rival banks are liquidating the same positions held by the same client is quite another.”

Archegos’ own “Lehman moment” came late on March 25 when…

Continue Reading